Part 3: Personal Savings

“According to the 2023 Statistics Canada report, 11.3 million tax filers contributed to either a Registered Retirement Savings Plan (RRSP) or a Tax-Free Savings Account (TFSA).[1]”

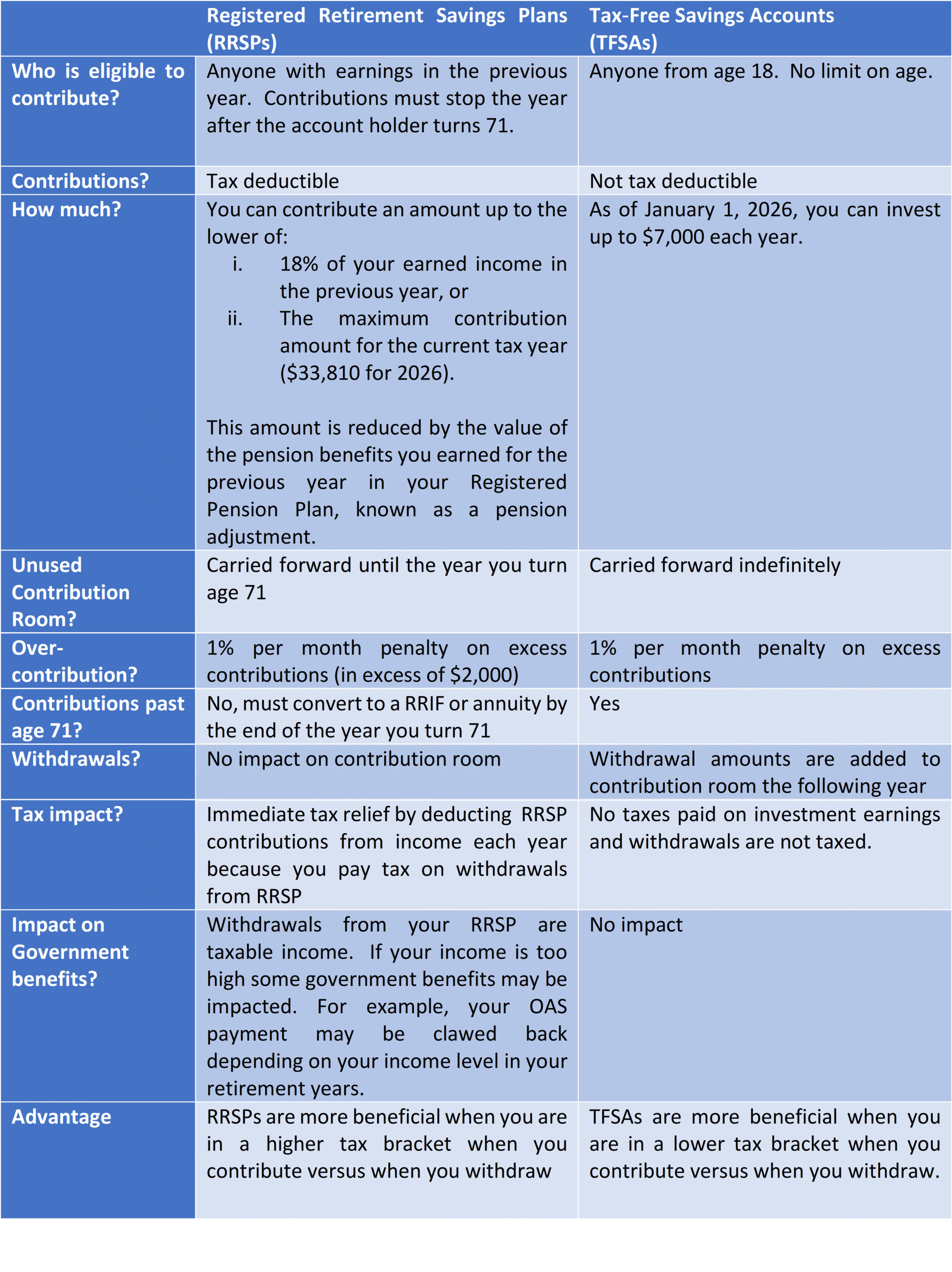

Part 1 of our 5-part series on Canada’s three-pillar retirement income system provided a general overview and Part 2 focused on how government benefits worked. Now in Part 3, let’s turn our attention to personal savings such as RRSPs and TFSAs, which are investment vehicles designed to help Canadians with their personal savings for retirement:

When it comes to saving for retirement, it's never too early to start, and the earlier, the better. Life’s many financial commitments, like a mortgage, rent, car loans, insurance, childcare expenses, and the list goes on, can make it challenging to save for retirement. Have a plan, make a budget, figure out how much money you can afford to save for retirement, and how much money you might need at retirement.

You may wish to seek the guidance of a financial advisor to help you figure out how to budget and which savings vehicle to use.

Part 3 of our series delved into the details of a couple of personal investment savings vehicles designed for retirement.

Check this website for the rest of our 5-part series on the retirement income system.